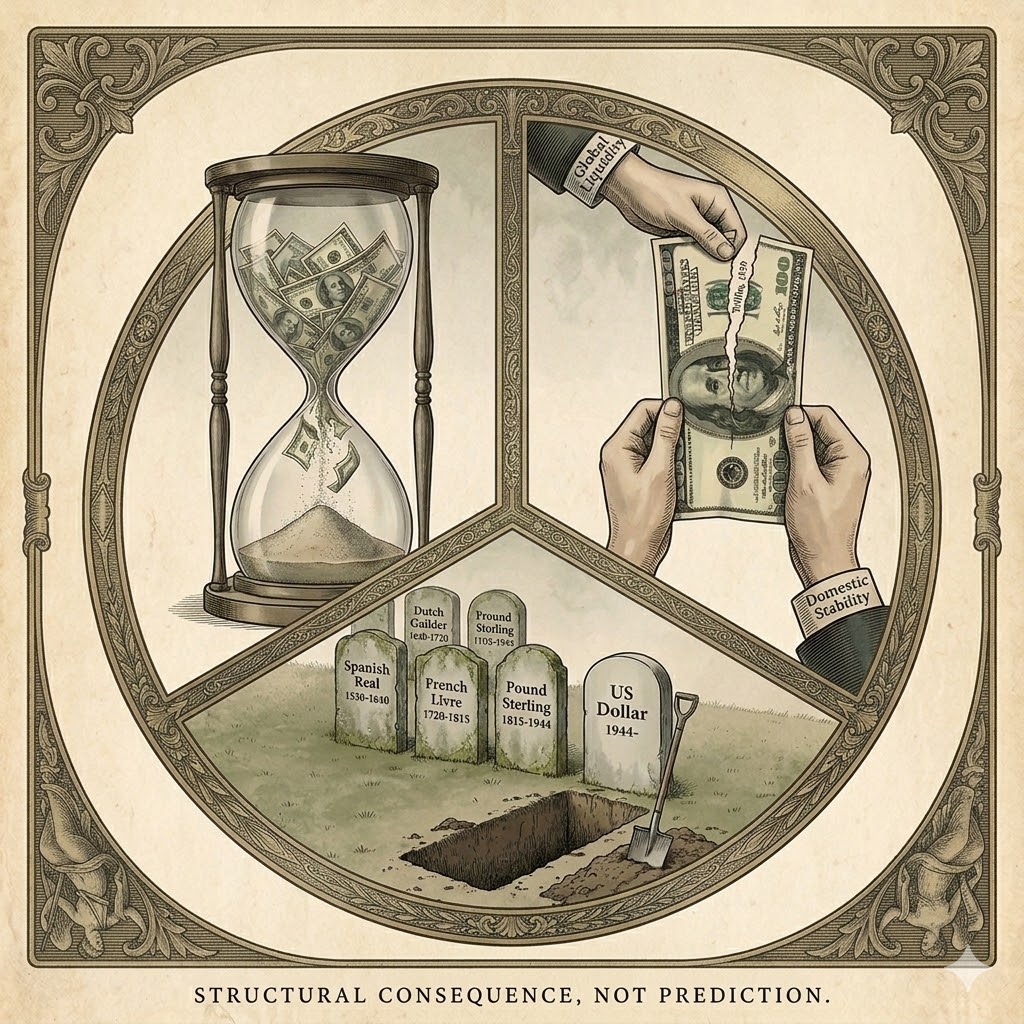

The Dollar's Expiry Date

The dollar-based international order is ending. Not as a prediction but as the structural consequence of choices made in 1944, accelerated in 1971 and triggered in 2022. The question is not whether it ends but how fast and whether countries build sufficient independence before the terminal condition arrives. This is the short version. The full strategic analysis, with sources, challenge points and adversarial testing, is here.

1944: the original choice

At Bretton Woods, Keynes proposed the Bancor. A neutral supranational unit of account managed by an International Clearing Union that would prevent any single nation from accumulating the structural advantages and vulnerabilities of reserve currency status. The United States, holding overwhelming economic and military dominance, overrode Keynes. The dollar became the global reserve currency. National advantage over systemic stability. Every subsequent problem flows from that choice.

Dollar reserve status gives the United States the exorbitant privilege: automatic demand for dollars and Treasuries, the ability to run deficits that would destroy any other currency, cheap borrowing. But the Triffin Dilemma is active from inception. To supply enough dollars for global reserves and trade, the US must run persistent current account deficits. It must spend more than it earns. Permanently. The privilege and the vulnerability are the same mechanism.

1953-1971: the designed destruction

Friedman’s 1953 essay “The Case for Flexible Exchange Rates” was not reactive analysis responding to system failure. It was the opening move in a sustained project to destroy a functioning system that constrained market forces in ways its architects opposed. The campaign lasted 18 years.

It was housed within the Mont Pelerin Society, founded in April 1947 by Hayek, with Friedman among the 39 founding members. Not an academic debating club. The William Volker Fund financed the inaugural conference. Credit Suisse covered 93% of its costs. The Society’s members founded the think tanks that provided the intellectual infrastructure for the revolution that followed: the IEA (1955, Antony Fisher at Hayek’s direct encouragement), the Heritage Foundation (1973), the Adam Smith Institute (1977), the Cato Institute (1977), the Atlas Network (1981, Fisher again).

Friedman stated the strategy explicitly: “Only a crisis, actual or perceived, produces real change. When that crisis occurs, the actions that are taken depend on the ideas that are lying around.” Twenty-five years ensuring their ideas were the ones lying around. This is not inference. It is documented purpose: identifiable donors, academics, think tanks and policy outcomes.

George Shultz (University of Chicago, Mont Pelerin member) became Nixon’s Treasury Secretary in June 1972. Friedman advised Nixon informally. Both advocated floating exchange rates. On 15 August 1971, Nixon unilaterally suspended dollar-gold convertibility. By 1973, the fixed exchange rate system had collapsed entirely. External discipline gone. The US could now create dollars without limit. This felt like freedom. It was the beginning of the terminal condition.

1973-1979: the crisis they caused, the cure they sold

OPEC reduced supply in 1973. That was not caused by the Chicago school. The vulnerability to it was. Floating currencies were hit far harder than pegged ones would have been. Exchange rate instability amplified a supply shock into currency crises. The UK went to the IMF in 1976 for a $3.9 billion loan, the largest in IMF history at that time.

Britain was damaged less by its own fiscal management than by the destruction of the international monetary framework within which that management had succeeded for 25 years. The resulting crisis was attributed to Keynesian management rather than to the destruction of Bretton Woods. The Chicago school’s further prescriptions (monetarism, central bank independence, fiscal austerity) were adopted as the cure for damage the first prescription helped create.

1979-1997: the lock-in

Thatcher arrived in 1979 with IEA briefings and Hayek’s The Constitution of Liberty as her declared intellectual foundation. She famously slammed the book on a policy meeting table declaring “this is what we believe.” Friedman advised directly. Reagan arrived in 1981 with Heritage Foundation policy papers. Twenty-two Mont Pelerin members were among his 76 economic advisers. Monetarism, central bank independence, fiscal rules constraining democratic fiscal management. Brown granted Bank of England operational independence in May 1997 (Bank of England Act 1998). The ideas that had been “lying around” were now load-bearing walls. The ideological project was no longer advocacy. It was the operating system of Western economic governance.

Every link in this chain is documented. Every actor is identifiable. Every think tank’s funding is traceable. These are not secret documents. They are public records that orthodox economics simply declines to read as a connected sequence.

The 50-year free lunch

Without the gold anchor, every administration discovers deficit spending is costless short-term. Reserve status absorbs the excess. Bush tax cuts. Iraq and Afghanistan. Financial crisis bailouts. Covid stimulus. Trump tax cuts. No political incentive to stop because the short-term cost is zero.

Interest payments reach roughly $1 trillion annually by fiscal year 2025. Debt sits at roughly 100% of GDP, projected to reach 120% by 2036. The deficit is $1.9 trillion with no politically viable path to reduction. The framework installed by Mont Pelerin forecloses every correction. Tax rises are ideologically toxic. Entitlement reform is politically suicidal. Defence cuts are geopolitically impossible.

2022: the trigger

In February 2022, the US and allies froze roughly $300 billion of Russian central bank reserves. Every non-allied sovereign drew the same conclusion simultaneously: dollar-denominated reserves are political instruments, not neutral stores of value. Central banks purchased over 1,000 tonnes of gold annually from 2022 to 2024, demand driven by strategic allocation rather than investment returns. The pace slowed in 2025 but the direction did not reverse. Not market sentiment. Sovereign strategic decision.

A self-reinforcing loop is now active. Reserve erosion, slower in the headline data than in the underlying sovereign decisions driving it, reduces automatic Treasury demand. Yields rise. Debt service increases. Deficits widen. Reserve status erodes further. At current debt levels, every percentage point on the federal funds rate translates into a fiscal event of enormous scale. The room narrows with every issuance cycle.

Four speeds to the same place

I model four trajectories in the full analysis: managed multipolarity, accelerated fragmentation, American reassertion and domestic fracture. Not four destinations. Four speeds toward the same one: the end of dollar-centric unipolarity and the emergence of a messier, multipolar order.

The erosion might have remained gradual. What compresses the timeline is the simultaneous degradation of the institutional credibility that sustained confidence in the system. The full analysis examines this in detail.

The strategic question is not which trajectory the US is on. It is whether other countries (particularly the UK) build sufficient institutional independence before the terminal condition arrives. Nations are building from the bottom up (through CIPS, mBridge, BRICS institutions, bilateral swap lines, gold accumulation) what the United States refused to build from the top down in 1944. Messier than the Bancor. Slower. But structurally inevitable given the logic set in motion 80 years ago.

The complete circle

Keynes was right. The United States chose national advantage over systemic architecture. The Mont Pelerin project removed the constraints. 50 years of consequence-free borrowing followed. The weaponisation of the system in 2022 triggered the strategic response now eroding the reserve status that funded the deficits. The consequences are arriving. Now.

The full strategic analysis, with sourced evidence, challenge points and adversarial testing, is here.